Overview

It's official: the Federal Reserve announced on November 3rd that it will create approximately $600 billion of new money to fund US Treasury bond purchases, and will also utilize another $250-$300 billion of money that had been previously created (also out of the nothingness). The usual term in the media for these planned purchases is "QE2", as in the second round of quantitative easing.

The "2" in "QE2" implies that this is something that has been done before. This implication is dead wrong.

"QE2" is radically different – and radically more dangerous – than the risky games that were played with earlier "quantitative easings". The Fed's current actions are all too likely to go down into financial infamy, and this brief article is intended to warn readers about some of the key differences this time around.

The most significant difference is that this time there appears to be no references to "sterilization" of the newly created money. It's likely good old-fashioned monetization in other words, with potentially quick and dire results.

It is also essential to note that the Fed won't be directly buying Treasury bonds from the US Treasury, but will instead be intervening in the Treasury bond markets. In other words, the Fed will be creating an artificial Treasury bond market, where it uses an unlimited amount of newly created public money to buy from private investment banks.

No Apparent "Sterilization"

As I wrote about extensively earlier this year, the previous "quantitative easing" (which means exactly the same thing as directly creating vast sums of money out of thin air, but sounds more responsible) has been done by the Federal Reserve and European Central Bank in a manner which economists refer to as "sterilized". This concept is confusing to most people, and I do my best to explain the process in understandable terms in the three articles linked below.

The Federal Reserve directly creates money in whatever volume it feels like - no need for borrowing despite the common myth - through creating "excess reserve balances" and using that new money to pay banks for securities purchases, as explained in "Creating A Trillion From Thin Air."

https://danielamerman.com/articles/Trillions.htm

However, while a (desperate) central bank wants to be able to spend money without limits, letting that new money escape into the general money supply can lead to major inflation in a hurry. So with the previous rounds, the Fed and ECB each used their "sterilization" powers to essentially put a corral up around the new money, and keep it from escaping out into the economy, as described in my article "Containing Inflation Via Unlimited Monetary Creation".

https://danielamerman.com/articles/Containment.htm

This "magic" process of "painlessly" creating trillions of dollars to bail politically connected banks out of their mistakes is far from free, and besides the enormous risks to the general population and the value of their savings, has the nasty side effect of effectively "hollowing out" the real economic basis underlying the banking system. This is because the banks can't really spend their "sterilized" money, but must have an ever larger share of their balance sheet assets consist of those economically meaningless excess reserve balances, as described in my article "The Fed's Hollowing Out Of US Banks".

https://danielamerman.com/articles/Hollow.htm

Now, when central banks create vast new sums of "sterilized" money, they are usually very, very careful to emphasize that the new money can't escape into general circulation. They do this to reassure the markets and their trading partners that their currency isn't (they hope) about to implode in value in an inflationary meltdown.

I've carefully studied the Federal Reserve statement of November 3 that described the Treasury bond purchase program. I studied Bernanke's detailed October 15 speech about the upcoming "nonconventional" steps which the Fed would be taking. I read Bernanke's simplistic public explanation of the actions in yesterday's Washington Post. There were a number of phrases that could be interpreted in different ways – but there was no direct reference to the sterilization of these funds. There were no promises that the funds would be kept out of the money supply. I'm profoundly skeptical that this lack of direct mention was some sort of omission.

Instead, it is a powerful offensive weapon in a currency war.

Keep in mind, that this has always been a monetization designed to meet multiple purposes. As covered in my article of two weeks ago, "Falling Dollar Means Rising Consumer Price Inflation", in an effort to revive the failing US economy, the US is attempting to slash the value of the dollar compared to other world currencies. If this can be done without setting off a wide scale currency war, then US jobs are helped in two ways, as the weaker dollar means that US exported goods become relatively cheaper and thus win more business overseas, even as the weaker dollar removes the artificial advantage that China and other nations have had in exporting their goods into the US.

As Chinese and other imported goods rise in price, they would lose market share, with the sales going to US based companies. The eventual goal would be for US workers producing US goods to fill the shelves of Wal-Mart rather than China doing so (which also necessarily means these goods cost more than they do today).

The threat that has successfully driven down the value of the US dollar since September is now being used in practice. Despite the doublespeak official announcements that you may read in the papers, this is a communication between central banks, and everyone involved knows what's going on. The US is threatening inflation that will drive down the value of its currency, making other nations unwilling to hold dollars, the lack of demand drops the value of the dollar relative to those nations' currencies, with benefits passing through to US companies that then hopefully revive the US economy - albeit at a terrible cost to US savers, and older Americans in general.

Spending Real Money

In evaluating why this so-called "QE2" is so different from the first rounds of quantitative easing, we need to understand that the use of the funds is quite different. In the autumn of 2008 the Federal Reserve used the original round of money to create artificial liabilities when there were no lenders, thereby keeping the highly leveraged banking system from collapsing. The money wasn't actually being spent on anything you could reach out and touch; this was more about balance sheets and accounting manipulations on a massive scale.

During 2009 and early 2010, for the true second round of quantitative easing (which involved rolling the new dollars over from the first round of bank loans and creating substantially more new dollars), the Federal Reserve created an artificial mortgage market, so that mortgage interest rates would be lower than what a free market would've allowed, and thereby would hopefully help slow down or avert a collapse in the housing market. The new money was used to acquire financial instruments (mortgage securities), but "sterilization" meant that the newly created money would not be allowed to escape from the Federal Reserve's and banks' balance sheets. So again, the new money wasn't being used to buy or create anything you could actually reach out and touch. The mortgage money had already been lent by the bank, so the newly created Fed money didn't go to the home purchasers.

What makes this current round night-and-day different is that the new money is being created to pay real people for real jobs and real tangible goods. The United States government budget deficit is not about market values of financial instruments, but rather about paying workers on a massive scale for "stimulus" projects. It's about massive road reconstruction projects and expensive high-speed rail lines – with the money being given to workers to go out and spend, in return for their labor. It's about paying a vast army of federal workers - who spend their paychecks. The federal budget deficit is about massive transfers and redistributions of wealth within the US, including Social Security and Medicare, low income housing and many other purposes. All of which require real money that really gets spent by real people.

This is about "stimulating" the economy, not sterilizing the hidden bailout funds. "Stimulating" means the money reaches the economy.

In other words, this money goes directly into the general money supply at a rate of about $110 billion per month through at least June, (the money is the sum of the to-be-created $600 billion, and the cash flow from the Fed's mortgage security portfolio that was purchased with created money). This adds up to lots more newly created government dollars chasing the same goods and services, and competing with savings earned over a lifetime.

There are about 111 million US households, so $110 billion per month in government spending funded by direct monetary creation is equal to about $1,000 a month per household in new money that is competing with our salaries and savings. And add another $1,000 in government money the next month. And so forth.

Another way of looking at this is that with an annual economy of a little over $14 trillion, total private and government spending runs about $1.2 trillion per month. Creating $110 billion a month in new money for the government to spend, means that about 9% of the economy will be purchased by newly created dollars. So 9% of purchases in this new economy would be made by brand new dollars, competing with and just as good as yours and mine, being spent for whatever purposes the government desires.

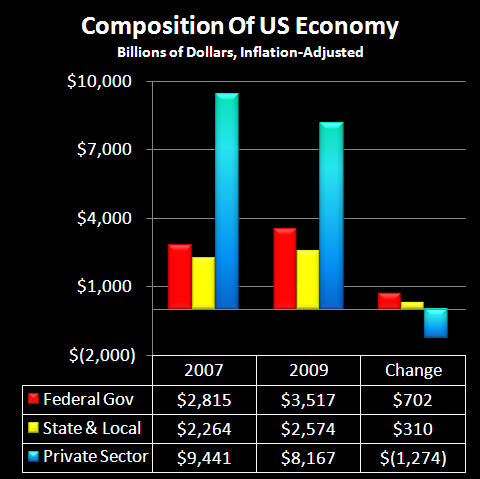

Some commentators are already noting that the Fed's plan would buy about the same amount of US Treasury bonds as net new Federal borrowing, meaning the entire US government budget deficit is being covered by the Federal Reserve's manufacturing new money, month by month. That is an interesting coincidence, isn't it? However, there is a much more fundamental "coincidence" at play here. The graph below is from my article "Soaring Government Spending 'Crowds Out' Private Investment Returns":

https://danielamerman.com/articles/Crowding.htm

Understand the graphs above and below, and you will see the heart of what is happening. Even using (suspect) official government statistics, the damage to the private sector has been catastrophic. The private sector shrank by .3 trillion between 2007 and 2009. But the economy "only" shrank by 0 billion. The difference was "covered" by an explosive growth in government spending, with federal, state and local government spending rising by trillion per year - at a time when tax revenues were falling.

This is no mere recession, and it is only massive government growth that has kept the plausible deniability in place. In two years, the government's share of the economy grew by 8%, from 35% to 43%. Without this fundamental change in the economy - which destroys the very basis of conventional stock market investing, as explained in the linked article - the US economy is in a collapse scenario.

What the Federal Reserve is doing is directly creating money equal to 9% of the economy, to artificially increase the government's share of the economy by 9%. It is artificial money for an artificial economy to avert collapse. With again, the night and day difference between this monetization and previous "quantitative easing" being that this new money is going directly into the economy, and competing with your money and your savings.

The only way out, as the government may be belatedly realizing, is to grow the real US economy. But you can't grow the real economy when the dollar is too high, because of currency manipulations by other countries. US goods become too expensive to export, even as domestic US industries are destroyed by subsidized foreign competition.

To grow the real economy - the value of the dollar must be slashed. Which, very conveniently, can be done through open monetization. So, you create vast sums of money out of thin air to artificially fund the economy, hoping to string things out as long as possible. Simultaneously, this very public monetization slashes the value of your currency, thereby stimulating real economic growth, which if you get really, really lucky, might grow the real economy fast enough to recover to a healthy level, and allow you to find an exit strategy from the insanely dangerous monetization policy before the value of the currency is annihilated.

That's the theory, anyway.

Not Direct Purchases, But Open Manipulation

There is something else essential for investors and savers to understand about the process which the Federal Reserve has just outlined. The Federal Reserve is not directly purchasing treasury bonds from the US government. Instead, US banks are purchasing the bonds from the US Treasury to fund the deficit, and then selling an equal amount of other bonds (likely at a nice profit) to the Federal Reserve. It would be reasonable to get annoyed at what appears to be the Fed's paying banks additional money to do effectively nothing, but to do so would be to miss the real point of this arrangement and the real danger.

To understand, let's explore what would happen if the Federal Reserve directly bought bonds from the Treasury (with appropriate legal changes if needed), but did not intervene in the Treasury bond markets. If there were a free bond market that was controlled by the self-interested investment decisions of private US investors (the foreign central banks and investors having fled because of Federal Reserve actions), then these investors might look at the Fed directly monetizing and say "I don't think I am being adequately compensated for my risk." And next thing you know, Treasury bonds might be going for 10% yields, or 15%+ yields. With ripple effects almost instantly going out into all interest rates throughout the US economy.

That's not what's going to happen (or apparently not yet, anyway).

Instead, the Federal Reserve, with effectively unlimited money at its disposal (targets can always be changed), can intervene at any time it wishes, in whatever volume it wishes, to make sure that Treasury bond and bill prices and yields are exactly what the Fed wants them to be. The US Treasury bond market then becomes an artificial market, much like the US mortgage market, with no connection to objective reality, and no discipline when it comes to the relationship between irresponsible government behavior and interest rates.

The private investors in the market play along, and maybe even increase their investments, because they understand that their "counterparty" can create money at will, and therefore (from a short term and terribly flawed perspective) it may look like risk-free profits. So long as they play along with the Fed.

If bond traders go the other direction, and speculate against the Fed - the Fed crushes them with its control of the market. In an openly and massively manipulated market, the governing factor is not theoretical fundamentals, but playing ball with the manipulator, and cooperating for your share of the rigged "profits".

What this means – for so long as this farce can hold together – is that there are no checks and balances on government spending, or on the share of the US economy that is controlled by the US government.

Even over the medium term this is a disaster scenario. But over the short term, it holds the game together for an increasingly desperate Federal Reserve and US government. Treasury yields ripple throughout all borrowings, and it is this absolute control of treasury yields that allows the Federal Reserve to keep interest rates low regardless of real inflation levels, even as stimulus funds continue to flow in unlimited volume, and regardless of what is happening with real wealth in the real US economy.

If you are a native-born US citizen – there's nothing "2" about this.

We've never seen anything like this in our lifetimes.

Similar things have happened in the world enough times before, however, even if the words "quantitative easing" were never used.

Many nations have been here before – and watched the value of their currencies collapse. The creation of "free" money that is so attractive to politicians for a brief period of time, becomes the most expensive possible way of funding government expenditures. Particularly for the savers, and especially the older savers, who see their life savings wiped out as a result of these grossly irresponsible actions.

What If The New Cash Is Sterilized?

The Fed has been deliberately vague about how exactly it will handle this program, which leaves open the possibility that the Fed could "sterilize" the new cash, or partially sterilize, or sterilize future purchases for future months.

The problem with this approach is that it effectively leads to the rapid systemic destruction of the economic basis of the US banking system, and also worsens the situation in the private sector of the economy. As covered in my "Hollowing Out" article linked above, by the end of the Federal Reserve's mortgage security purchase program (the previous "quantitative easing"), about 10% of the approximately trillion in US banking system assets consisted of sterilized money held at the Federal Reserve. The Federal Reserve is committed as a matter of policy to keeping this money from escaping into general circulation – effectively preventing the bank from actually lending it out to a company for instance.

New monetary creation at a rate of approximately 0 billion per month is equal to a monthly volume of about 1% of total banking assets. The announced program, if "sterilized", would mean that by June, about 16% of total US bank assets would consist of "sterilized money", i.e. balances at the Federal Reserve that can't be used anywhere else.

Another way of phrasing this is that the US government budget deficit would be funded by essentially "taking" 1% of the assets of the US banking system every month, and using that to cover the excess US government spending. How this works is that in the first month, the primary dealer banks would purchase 0 billion in newly issued Treasury bonds, and would sell 0 billion in already existing Treasury bonds to the Federal Reserve. The Fed would pay for the bonds with money newly created on the spot – but because the money has been "sterilized", the 0 billion in sale proceeds isn't really spendable by the selling bank. The actual Treasury bonds bought and sold are different. It would be pure coincidence if the sector of the bond market whose prices and yields the Fed was most interested in manipulating that month were to match what the Treasury department was selling (and there is no need for dates or dollar amounts to precisely match up).

The following month, when the primary dealers purchase another 0 billion of newly issued Treasury securities to fund the Federal budget deficit, they don't have access to the 0 billion from the previous month (*), so they have to take a new 0 billion out of their other assets to purchase the new bonds. They also make the sale of 0 billion of whatever already outstanding Treasury bonds the Fed is most interested in manipulating the price of that month, and the Fed pays them a nice price, but they have to leave the 2nd 0 billion in sale proceeds at the Fed too (it's not technically mandatory, but Bernanke is proud of the tools he uses to sterilize the cash, as covered in my "Containing Inflation Via Unlimited Money Creation" article). (*) If they did use the previous month's Fed payment to buy new Treasury bonds, then it is a direct monetization scenario, not a sterilization scenario.

So now the banking system is out 0 billion in terms of accessible cash, and when the third month's 0 billion of Treasury bonds needs to be bought, that can't come from the newly created Fed money either. Which means another 0 billion has to come out of other assets of the US banking system.

This rapid hollowing out of the US banking system to fund a voracious and apparently never-ending federal deficit, where every month a greater share of banking assets becomes the debt of a bankrupt government, is obviously a dangerous strategy that grows more likely to blow up each month it is employed. It also means that with each month, there are less banking assets available to be lent to businesses and consumers, which then makes economic recovery that much less likely. In other words it would be an insane strategy for a government that is desperately trying to revive the private sector economy, which is one of the reasons I find further sterilization to be unlikely.

With the much more likely monetization scenario, the Fed purchases from the primary dealers 0 billion in whatever Treasury bonds it is most interested in manipulating the price of, in order to control interest rates. The primary dealer banks take the 0 billion, which is non-restricted (as it isn't sterilized) and buy 0 billion of that month's new Treasury bond issuance. Because the bank cash flow between buying and selling is a wash (except for their profits on each side), from a cash flow perspective this is the same as the Federal Reserve directly creating money to buy all newly issued Treasury bonds. However, the advantage to doing it this way, as previously discussed, is that the Fed not only directly funds the deficit, but it takes direct control of the Treasury market, which more or less translates to direct control over most US interest rates.

As for what the Fed is doing – Bernanke is effectively mumbling when it comes to the explanations. He's being careful not to be clear, so he can claim to have his cake and eat it too (maintaining even a semblance of plausible deniability is also very important in the diplomatic maneuverings accompanying the nascent currency war). As explained above, when the central bank creates vast sums of new money – and doesn't explicitly say it is "sterilizing" – the odds are quite high that in fact, it is not sterilizing. But even if it is sterilizing, the results of this unprecedented monetary creation still lead to another disaster scenario. Further sterilization accelerates the collapse of the private sector and banking system in real terms, which must then be covered by still more monetization.

It has to be one or the other: either newly created money is going directly into the economy in straight up monetization, or the assets of the US banking system are being sucked out by the voracious Federal Government deficit at a very fast rate, leaving a hollow shell. What the Fed is doing to the banks with sterilization is much like a spider consuming an insect: punching a hole in the exoskeleton with its fangs and sucking the innards out, while the exoskeleton remains an intact but hollow shell. (For those who would say the Fed would never do that to the banks that run it - the Fed has already been doing it, and don't forget the crucial distinction between the interests of the banks and the personal financial interests of the senior executives who run the banks.)

Either about ,000 a month per US household is being created and spent in the economy in direct monetization, competing with your dollars and savings - or about ,000 a month per US household will be sucked out of the banking system by the government through sterilization, meaning less money for business and consumer lending, and an acceleration in the decline of the real economy. The former in my opinion is the much more likely route, and represents a radical change, but either way, there is no such thing as "free money", and the piper will be paid. By all of us.

Finding Refuge

We have a good idea of the path ahead - which is the destruction of the value of the currency, as well as the impoverishment of a good part of the population. By far, the heaviest punishment will fall on the older members of the population whose savings are destroyed, and who do not have the remaining years to recapture what they have lost.

There are solutions, and not everyone will see their savings destroyed. By taking the right series of steps, assets can be preserved – or even expanded, even in after-inflation and after-tax terms. The difference between being destroyed, and saving your assets, quite simply comes down to a matter of making informed decisions. It is a matter of education, in other words.

A good starting step is to read and understand the three articles linked earlier in this article which cover the essentials of direct monetary creation, sterilization, and hollowing out the banking system. I've done my very best to make these articles understandable, and from the feedback which I received at the time they were published, these articles provide valuable new insights into what is really happening and what the central banks have really been doing.

When it comes time for action, the simple and increasingly popular solution is to pull all you can out of paper investments and symbolic currencies, put them in gold, and hunker down to survive the storm that is building in strength by the week.

Unfortunately, however, we live in a complex and deeply unfair world, that makes mincemeat of emotional reactions and simple solutions. As illustrated in step-by-step, easy to understand – but irrefutable – detail in the article "Hidden Gold Taxes: The Secret Weapon Of Bankrupt Governments" (linked below), a simple solution of just buying gold leaves you handing a good chunk, or perhaps most of your starting net worth, over to the government by the time all is said and done. The way the government – under existing laws – effectively confiscates the wealth of gold investors in a highly inflationary environment is little understood by most gold investors, but should form the central point for their investment strategies.

https://danielamerman.com/articles/GoldTaxes1.htm

Let me suggest an alternative approach, which is to study, learn and reposition. To have a chance, you must learn not just how wealth will redistribute, but how unfair government tax policies (that can be relied upon to increase in unfairness) will cripple most simple methods of attempting to survive inflation.

Then, yes – buying gold (and perhaps a lot of it) can be one key component of a portfolio approach, as discussed in my Gold Out-Of-The-Box DVD set. Use multiple components, each doing what they do best, shift the components in a dynamic strategy over time, and position yourself so that wealth will be redistributed to you in a manner that reverses the effects of government tax policy. So that instead of paying real taxes on illusionary income, you're paying illusory taxes on real income. And the higher the rate of inflation and the more outrageous the government actions – the more your after-inflation and after-tax net worth grows.

Best wishes to you in these perilous times.

Do you know how to Turn Inflation Into Wealth? To position yourself so that inflation will redistribute real wealth to you, and the higher the rate of inflation – the more your after-inflation net worth grows? Do you know how to achieve these gains on a long-term and tax-advantaged basis? Do you know how to potentially triple your after-tax and after-inflation returns through Reversing The Inflation Tax? So that instead of paying real taxes on illusionary income, you are paying illusionary taxes on real increases in net worth? These are among the many topics covered in the free “Turning Inflation Into Wealth” Mini-Course. Starting simple, this course delivers a series of 10-15 minute readings, with each reading building on the knowledge and information contained in previous readings. More information on the course is available at DanielAmerman.com or InflationIntoWealth.com .

Contact Information:

Daniel R. Amerman, CFA

Website: https://danielamerman.com/

E-mail: mail[at]the-great-retirement-experiment[dot]com

This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.