There is no doubt the home price bubble inflated by Alan Greenspan between 2000 and 2006 was the Mother of All Bubbles. Robert Shiller clearly showed that home prices were two standard deviations above expectations. Despite the unequivocal facts that Dr. Shiller put forth, millions of delusional unsuspecting dupes bought houses at the top of the market. These were the greater fools. They actually believed the drivel being spewed forth by the knuckleheaded anchors on CNBC. They actually believed the propaganda being preached by David Lereah from the National Association of Realtors (Always the Best Time to Buy) about home prices never dropping. They actually believed Bennie Bernanke when he said:

"We've never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don't think it's gonna drive the economy too far from its full employment path, though." – 7/1/2005

“Housing markets are cooling a bit. Our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise.” – 2/15/2006

Bennie actually made these statements when the chart below showed home prices at their absolute peak. You should keep this in mind whenever this rocket scientist opens his mouth about anything. And always remember that he is a self proclaimed “expert” on the Great Depression. That should come in handy in the next few years, just like his brilliant analysis of the strong housing market.

Source: Barry Ritholtz

Alan Greenspan created the Mother of All Bubbles by keeping interest rates at 1% for a prolonged period of time while encouraging everyone to take out adjustable rate mortgages. His unshakeable faith in the free market policing itself allowed Wall Street criminals, knaves and dirtbags to create fraudulent mortgage products which were then marketed to willing dupes and “retired” internet day traders. Al’s easy money policies and disinterest in enforcing existing banking regulations also birthed the ugly stepsister of the Mother of All Bubbles. Her name is the Consumer Debt Bubble. The chart below is hauntingly similar to the home price chart above. The consumer will be deleveraging for the next ten years. The numbskulls on CNBC and the other mainstream media have been falsely reporting for months that consumers were deleveraging when it was really just debt being written off by banks. Baby Boomers are not prepared for retirement and will be shifting dramatically from consuming to saving. As consumer expenditures decline from 70% of GDP back to 65% of GDP, consumer debt will resemble the home price chart to the downside.

The savings rate has soared all the way to 6% of personal income. This is up dramatically from the delusional boom years of 2004 and 2005 when it bottomed out at 1%. It ain’t even close to being enough to fund the looming retirements of the Baby Boomers. The savings rate averaged 10% from 1959 through 1989. In order for the American economy to revert to a balanced state where savings leads to investment which leads to wage increases, the savings rate will need to be 10% again. With annual personal income of .5 trillion, Americans will need to save an additional 0 billion per year. This means 0 billion less spending at the Mall, car dealerships, Home Depot, tanning salons, and strip joints. Don’t count on a consumer led recovery for a long long time.

So here we stand, two years after the worldwide financial system came within a few hours of imploding, and nothing has changed. Wall Street is still calling the shots. The political hacks that supposedly run this country have kneeled down before their insolvent Masters of the Universe. Bennie Bernanke has chosen to save his Wall Street masters and throw grandma under the bus. By keeping interest rates at zero, buying up trillions in toxic mortgages, and printing money as fast as his printing presses can operate, Bennie has birthed the bastard child of the mother of all bubbles. The chart below clearly shows the birth of this bastard. It is a distant cousin of the internet bubble bastard. Despite interest rates at or near all-time lows across the yield curve, money has poured into Treasury bonds. This makes no sense, as interest rates can’t go much lower. A small increase in rates will produce large losses for investors at these rates.

Source: Barry Ritholtz

Only a fool would buy a US Ten Year Treasury bond today yielding 2.55%. Of course, only a fool would buy a 1,300 square foot rancher in Riverside, California for 0,000 with 0% down using an Option ARM in 2005 too. But that doesn’t mean there aren’t millions of fools willing to do so. Each “investment” will have the same result – huge losses. As anyone can see from the chart below, the 10 year Treasury has been in a 30 year bull market. At this point you have to ask yourself one question. Do you feel lucky? Well do you, punk? There are a number of analysts who see rates falling further as the economy sinks into Depression part 2. That may happen, but we all know that Bennie and those in power will do anything to avoid a deflationary spiral. That means looser money and more printing.

The Federal Reserve does not want a 20 year recession like Japan. They will not get it. They’ll get a hyperinflationary collapse instead. Japan entered their 20 years of stagnation with a population that saved 18% of their income and huge trade surpluses. The Japanese government could count on the Japanese population to buy every bond they issued to pay for worthless stimulus projects. The US has entered this Depression with a population that saved 2% of their income and a trade deficit of 0 billion. John Hussman describes the differences between the US and Japan in his recent newsletter:

The impact of massive deficit spending should not be disregarded simply because Japan, with an enormously high savings rate, was able to pull off huge fiscal imbalances without an inflationary event. We may be following many of the same policies that led to stagnation in Japan, but one feature of Japan that we do not share is our savings rate. It is one thing to expand fiscal deficits in an economy with a very elevated private savings rate. In that event, the economy, though weak, has the ability to absorb the new issuance. It is another to expand fiscal deficits in an economy that does not save enough. Certainly, the past couple of years have seen a surge in the U.S. saving rate, which has absorbed new issuance of government liabilities without pressuring their value. But it is wrong to think that the ability to absorb these fiscal deficits is some sort of happy structural feature of the U.S. economy. It is not. It relies on a soaring savings rate, and without it, our heavy deficits will ultimately lead to inflationary events.

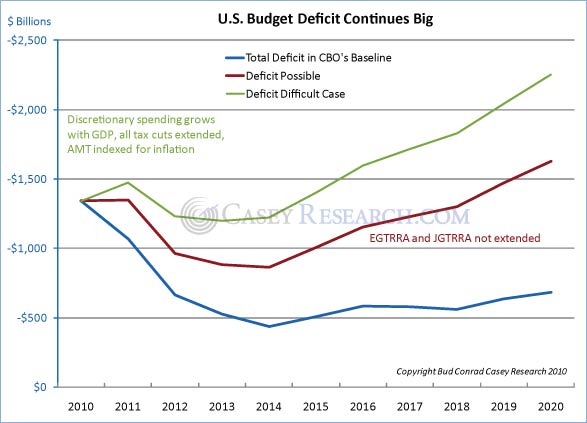

The child of the mother of all bubbles likes to live dangerously. Congress will surely extend all of the Bush tax cuts without restraining spending in any way. That is what they call compromise in the hallowed halls of the Capitol. By 2020 the National Debt would be Trillion under this scenario. Annual interest on the debt would exceed trillion per year. This is a death spiral scenario, but it is the path we are choosing. Again, I ask you, who in their right mind would buy a 10 Year Treasury bond yielding 2.55% when the US will either have a trillion National Debt or will have already collapsed under the weight of that debt?

Foreigners own approximately 30% of our outstanding debt. But, we have been relying on them to purchase almost 40% of our new issuance. We will need to issue trillion of new debt in the next two years. Foreigners can add. They see that we are on a course that isn’t sustainable. They know that the Fed will attempt to monetize our debt and weaken the USD over time. At 2.5% interest rates, foreigners will accumulate massive losses as the USD depreciates. They will not accept these low rates for much longer. It is a confidence game. As they lose confidence in our ability to confront our debt issues, rates will be forced higher.

The pollyannas that seem to proliferate on CNBC and the rest of the mainstream media declare that since interest rates haven’t spiked and our hyper-debt based financial system is still functioning, then there is nothing wrong. They also didn’t see the internet collapse, housing collapse or financial system collapse coming. They never do and never will. China has actually been selling Treasuries for over a year. Japan is still buying, but their far worse debt/demographic crisis will force them to curtail purchases of Treasuries in the coming years. The purchases being made from the UK are really purchases from Middle Eastern countries with their oil money. I wonder what would happen to these purchases if war with Iran breaks out? It seems we have foreign countries increasingly reluctant to buy our debt when we are about to issue trillions of new debt in the next few years and as far as the eye can see.

The only thing that could possibly keep foreigners buying our debt would be higher interest rates. Our economy is so saturated with debt from top to bottom, that an increase in interest rates of only 2% would have a devastating impact on our economy. John Hussman understates the impact of deficits on our economic future:

Continued deficits will have substantial economic consequences once the savings rate fails to increase in an adequate amount to absorb the new issuance, and particularly if foreign central banks do not pick up the slack. We’re not there for now, but it’s important not to assume that the current period of stable and even deflationary price pressures is some sort of structural feature of the economy that will allow us to run deficits indefinitely.

The Krugmans of the world are not worried about our debt. They say pile it on. We are America. We are the most powerful nation in the history of the world. We can obliterate any enemy with the push of a button. Why do we need to worry about some debt? This is the hubris that has led to the downfall of every great Empire. As Rogoff and Reinhart point out in their recent book, this time is not different:

“As for financial markets, we have come full circle to the concept of financial fragility in economies with massive indebtedness. All too often, periods of heavy borrowing can take place in a bubble and last for a surprisingly long time. But highly leveraged economies, particularly those in which continual rollover of short-term debt is sustained only by confidence in relatively illiquid underlying assets, seldom survive forever, particularly if leverage continues to grow unchecked.

“This time may seem different, but all too often a deeper look shows it is not. Encouragingly, history does point to warning signs that policy makers can look at to assess risk – if only they do not become too drunk with their credit bubble – fueled success and say, as their predecessors have for centuries, “This time is different.”

A tipping point is reached when the government debt exceeds 90% of GDP. US government debt is currently at 93% of GDP. One year from now it will exceed 100% of GDP. The bastard child of the mother of all bubbles has jumped out a window on the hundredth floor of a NYC mega bank. As he passes the 50th floor, Paul Krugman asks him how is he doing? He says great, SO FAR. We all know what happens next. SPLAT!