During the summer of this year I penned a discussion suggesting that we all watch durable goods orders (ex aircraft and defense spending) closely for clues as to how businesses were assessing and preparing for the Fiscal Cliff. At the time, I thought it a good bet that new orders would fall, and perhaps meaningfully, with no certainty regarding Fiscal Cliff outcomes. Not exactly the stuff of heroic prognostication or rocket science, clearly. Yes indeed, orders have fallen exactly as one would have expected in a period of legislative uncertainty. As of now, the year over year change in durable goods new orders (x-aircraft/defense) stands at a level usually reserved for recessionary periods.

Moreover, as per the latest GDP report, we’re also seeing weakness not only related to business spending (very slow advances in equipment and software spending – a proxy for business spending in the GDP report), but also related to consumers. Despite the higher headline GDP number for the 3Q, the latest revision saw a reduction in personal consumption and business spending relative to the prior report. The perversity of higher inventories added to the perceptual headline gain for GDP.

One data point I continually check in on at each GDP report is real final sales to domestic purchasers. Reason being this number IS GDP, but stripped of the influence of inventories and foreign trade. Of course when looking at the very long term rhythm here, it’s unmistakable that the current is the most “soft” recovery really in the history of the data. Exactly what one would expect in a generational deleveraging cycle.

So back to the issue at hand that is manufacturing. Remember, manufacturing has been a big bright spot in the current recovery. I have written in these pages about the historical anomaly that is the weak US service sector expansion in the current economic recovery cycle. Moreover, in missives past, I’ve also written about a mini manufacturing renaissance in the US in good part based on cheap(er) domestic energy sources looking into the years immediately ahead. To the point, the ISM number reported a few weeks back showed us the first break below 50 in the series since last summer. Again, this should not have been a surprise given the direction of durable goods numbers in recent months. But components of the report deserve comment. Looking at the components forced me to ask myself, has the moment of truth for manufacturing in the current cycle arrived? I think it has. Key question being, with the very meaningful rate of change slowing in US goods exports, can the US domestic economy specifically pull a greater GDP load ahead and much of that based on manufacturing? Let’s look at a few of the very important “leading” components of the ISM report.

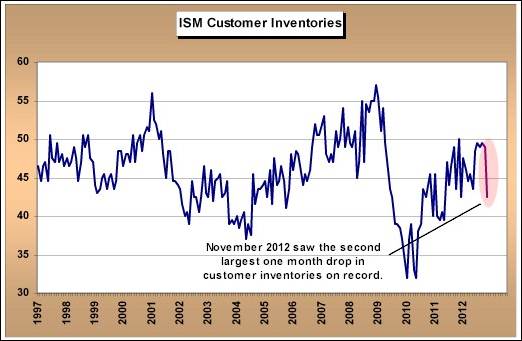

Here’s what really caught my eye. November saw the second largest one month drop in ISM customer inventories on record.

It just so happens that the largest one month drop was recorded in December of last year, but this came after a three month series of customer inventory numbers volatility that was a record for this data. We’ve seen no such prior monthly period strength to the upside as a counterpoint to the current decline, as was exactly the case in 2011. First, a decline in inventories is subtractive from headline GDP. So personally I expect this to weigh on 4Q macro US GDP when reported. Again, this should be no surprise at all.

Secondly, we know the Fiscal Cliff issues have weighed on business spending as is clearly seen in the durable goods numbers over the past three to six months. So as we look at the current ISM customer inventory data, the question now becomes, is the current period decline also in reaction to Fiscal Cliff worries, or is this something more, perhaps businesses looking beyond the fiscal cliff at the post-cliff realities of the domestic and global economies? I think this is a very important question as well as now forward data watch point of significance. The mainstream press has portrayed the environment of the moment as dependent on short term US Fiscal Cliff outcomes, without a lot of looking “beyond the Cliff”. Implication being that once Cliff issues are certain, businesses will once again resume expansion. If that is indeed to be the case, then shouldn’t inventory restocking in the manufacturing sector be a keynote feature of that expansion? Without question, as ISM customer inventories are simply too low for an expansionary macro environment.

One more quick ISM data point in terms of leading tendencies. New orders are certainly one of the most important leading components of the manufacturing report. Of course new orders fell in the current period as manufacturing sector customers engaged in “de-stocking” (the customer inventory numbers), only as one would expect. Over time the new orders to manufacturers inventories ratio has helped us get a feeling for forward strength or weakness to come. Are orders too high relative to inventories or too low? As it stands now, despite low customer inventories, the new orders to manufacturers inventory ratio is just a touch below the very long term average.

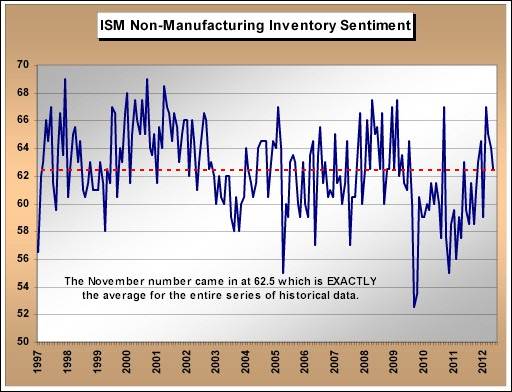

Meaning, there is not a lot of information here about where customer inventories may head in the future as the current reading above is not too hot or too cold. It’s the customers of the manufacturing sector we need to watch to get a sense for improved economic strength ahead or otherwise. And I’d stress the manufacturing sector because although the recent headline non-manufacturing (service sector) ISM number “beat the estimates”, the inventory sentiment number among service sector participants in November came in EXACTLY at the long term average of the entire history of the data. Inventories n the service sector are not depressed.

So, key message being, if we are going to see inventory rebuilding strength ahead, which would tell us businesses were expecting better days in the future, it will come from the manufacturing side of the economy and not the service sector. Important in that manufacturing sector reflects both the domestic as well as global economy. In other words, manufacturing reflects much more than simple domestic Fiscal Cliff fallout. Keep an eye on the ISM customer inventories number. I think it will be very important in trying to get a sense for post-Cliff economic reality.

Final comment that is really an update of a data relationship I track consistently. Hit tip to Francois Trahan at Wolfe Trahan for this one. It’s the average of the two headline ISM series set against the year over year change in the S&P (price only). Question of the moment being, will the rate of change in the S&P come down to meet the ISM series, or will both ISM series strengthen ahead to meet the rate of change in the S&P? The ISM customer inventory data point may be a tip off in the months ahead.