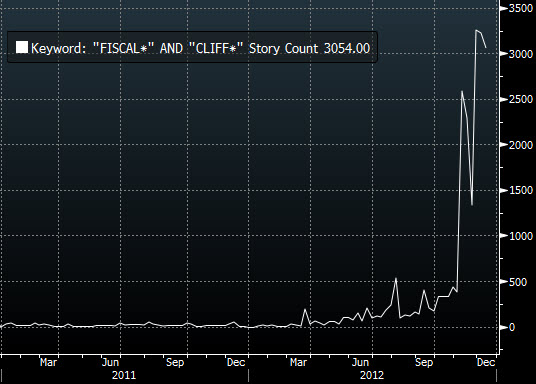

A simple glance at newsstands or listening in on TV news would make it clear that the fiscal cliff is the primary public obsession of the moment. Bloomberg’s news trend, which searches for keywords and plots story counts with those keywords, shows that the fiscal cliff obsession has hit a crescendo, which unfortunately is masking what is taking place globally, a re-acceleration in economic growth.

Source: Bloomberg

For much of 2010-2011 most global central banks were tightening monetary policy to cool overheated economies that became white-hot after massive global stimulus. Those actions achieved their purpose to a level where growth is more of a concern than inflation. In response we’ve now seen much of the globe ease financial conditions over the last twelve months and it appears to be finally paying off as global growth looks to pick up heading into 2013.

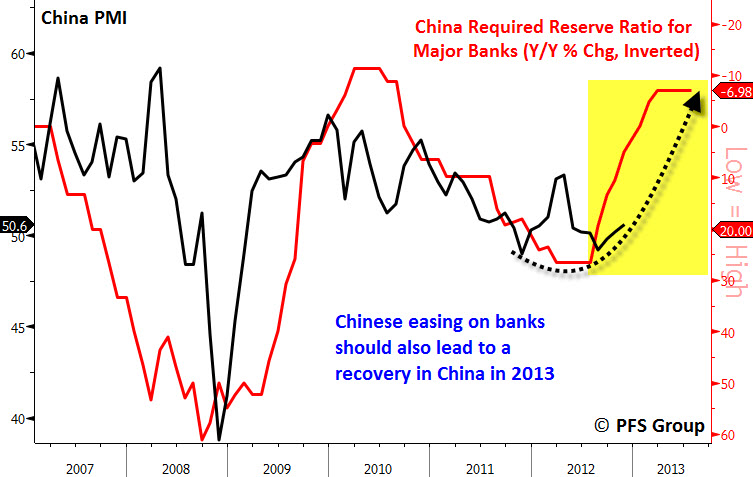

China, the world’s growth juggernaut, was widely feared to slip into a hard landing scenario as many doomsayers would have us believe. However, Chinese easing of bank reserve ratios is a strong leading indicator for manufacturing activity and suggests that the Chinese economy should pick up steam meaningfully in 2013 which will buoy global growth.

Source: Bloomberg

Similarly to China, easing in credit conditions in Europe is likely to be supportive of European economic activity in 2013. The Bloomberg European Financial Conditions Index (red, lower panel below) recently hit a 5-year high as credit conditions in Europe continue to improve.

Source: Bloomberg

A breakout to a 5-year high in the Bloomberg European Financial Conditions Index is particularly significant as, like the Chinese bank reserve ratio, easing in financial conditions leads economic activity and signals that Europe may be a global bright spot in 2013.

Source: Bloomberg

Even Japan, which has gone nowhere for longer than most can remember, may be set to get a boost from easy monetary policy that weakens the Yen and spurs exports. The Yen has weakened considerably relative to the USD and it looks like the 5-year run the Yen had relative to the USD is over, which is providing a lift to the Japanese Nikkei 225 Index.

Source: Bloomberg

If Japan’s recently elected leader Shinzo Abe has his way, Japan may be the global reflationary hot button in 2013 as an article from The Telegraph highlights:

Japan's Shinzo Abe prepares to print money for the whole world

Japan’s incoming leader Shinzo Abe has vowed to ram through full-blown reflation policies to pull his country out of slump and drive down the yen, warning Japan's central bank not to defy the will of the people.

The profound shift in economic strategy by the world’s top creditor nation could prove a powerful tonic for the global economy, with stimulus leaking into bourses and bond markets - a variant of the "carry trade" earlier this decade but potentially on a larger scale.

"We think this could be the beginning of a fresh reflation cycle for the global system, combining with the US recovery to mark a turning point in the crisis," said Simon Derrick from BNY Mellon.

"It is tremendously important for global growth, and markets are starting to take note," said Lars Christensen from Danske Bank.

Mr Abe’s Liberal Democratic Party (LDP) won a landslide victory on Sunday, securing a two-thirds "super-majority" in the Diet with allies that can override senate vetoes.

Armed with a crushing mandate, Mr Abe said he would "set a policy accord" with the Bank of Japan for a mandatory inflation target of 2pc, backed by "unlimited" monetary stimulus.

"Its very rare for monetary policy to be the focus of an election. We campaigned on the need to beat deflation, and our argument has won strong support. I hope the Bank of Japan accepts the results and takes an appropriate decision," he said.

The menace behind his words did not have to be spelled out. He has already threatened to change the Bank of Japan’s governing law if it refuses to comply. "An all-out attack on deflation is on its way," said Jesper Koll, Japanese equity chief at JP Morgan.

While fears of the U.S. going over the fiscal cliff are real, what is most likely to occur is some small package that averts most of the fiscal cliff impacts and buys time to deal with the upcoming debt ceiling and iron out further details. If it turns out that most of the fiscal cliff impacts will be averted, then it is fairly likely the U.S. will avoid a recession, particularly with global growth set to pick up steam. The U.S. is already on the mend from this summer’s malaise as the housing recovery continues to pick up steam and exerts its wide-ranging effects on the economy.

Probably chief among them is a rise in the U.S. consumer’s largest asset, their home. The NAHB Housing Market Index for December was released this week and it hit another new high. Given the Housing Market Index leads annual price changes in home values, we are likely to see national housing prices continue to rise into 2013. The more housing prices climb the more homeowners with not enough equity to refinance at historically low mortgage rates will be able to refinance as loan-to-value ratios decrease. Housing price appreciation is also directly correlated to consumer confidence and spending, with both likely following housing prices higher in 2013.

Source: Bloomberg

Source: Bloomberg

In addition to a housing recovery to continue in 2013, it looks like manufacturing may also receive a lift as incoming data this week was very encouraging. The American Institute of Architects Billings Index climbed to 53.2 last month to a 5-year high and logged its sixth consecutive gain, the longest winning streak in the 17-year history of the data (article link). The Billings Index tends to lead the ISM Manufacturing PMI by 1-month, which suggests we see a sharp rebound in the next ISM PMI reading.

Source: Bloomberg

Other data released this week pointed to improvements in the economy as the following Bloomberg article highlights:

Americans Look Past Fiscal Debate as Spending Climbs: Economy

Americans looked past the debate on fiscal policy in November as consumer spending and demand for durable goods climbed, indicating the economy strengthened heading into the current impasse on tax rates and spending cuts…

Wages Rebound

Wages and salaries also advanced 0.6 percent in November after falling 0.3 percent a month earlier. Because the increase in pay surpassed the gain in spending, the savings rate climbed to 3.6 percent in November from 3.4 percent the prior month.

Industry figures show car and light truck sales rebounded in November as buyers returned to showrooms following the storm. Light vehicles sold at 15.5 million annual rate last month, the most since 2008, according to data from Ward’s Automotive Group.

Durable Goods

The increase in demand for durable goods such as machinery and electronics in November showed companies were planning to expand next year as they looked beyond the tax increases and spending cuts slated to take effect.

Bookings for non-defense capital goods excluding aircraft, a proxy for future business investment, rose 2.7 percent last month after a revised 3.2 percent gain in October that was larger than previously estimated, today’s report on durable goods showed.

Shipments of those items, used in calculating gross domestic product, increased 1.8 percent in November, the biggest gain in eight months, after a 0.6 percent advance the prior month that was previously estimated as a 0.1 percent decline. The back-to-back advance indicates business spending is rebounding this quarter.

Summary

While all the focus is currently cast on the ongoing fiasco caused by our elected officials, the real story is the re-acceleration that is occurring in global growth as prior drags (China, Europe, and Japan) are set to become major supports. While some of the sting from the fiscal cliff is likely to curb U.S. growth in 2013, it looks like U.S. economic activity should stay strong enough to avoid a recession as housing continues to slowly improve and manufacturing recovers.