Originally posted at Briefing.com

Anyone who has been riding the wave of the S&P 500 information technology sector's outperformance must be feeling like the Big Kahuna. This past week, however, something happened to make one wonder if that wave is cresting.

One of the sector's most-loved stocks — Facebook (FB) — announced an astounding cut in its operating margin outlook that didn't register well with growth-oriented investors.

The price for that disappointment was steep indeed. Facebook saw its market value reduced by nearly $120 billion, earning it the ignominious distinction of incurring the largest single-day loss of market value in U.S. stock market history.

That loss — and the speed with which it occurred — opened the market's eyes to the crowded positioning in that specific stock and in the information technology sector in general.

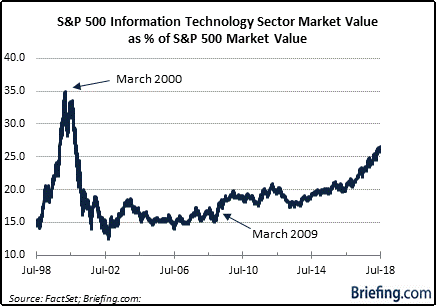

It is a crowd that has been building steadily for several years and which has pushed the sector's market weight as a percentage of the S&P 500's market value to its highest level since November 2000 when the information technology sector was still embroiled in the dot-com implosion.

If you think the information technology sector is over-owned today, however, the chart below will lend some visual perspective to the bacchanalian days of the dot-com bubble.

In March 2000, the information technology sector accounted for 35% of the S&P 500's market value. Facebook, by the way, didn't even exist then and Alphabet/Google was just getting started.

Times Change

Times do change and so do the companies in the information technology sector that roll with the times. A few days ago, Facebook had a market valuation close to 0 billion, while Alphabet/Google (GOOG), which was founded in 1998, had a market capitalization approaching 0 billion.

Apple (AAPL), meanwhile, was in the market's dustbin during the dot-com heyday, yet it is now the market's most valuable company, knocking on the door of a trillion market capitalization.

If you own an S&P 500 index fund or an ETF like the SPDR S&P 500 ETF (SPY) or the Invesco QQQ Trust (QQQ), you own these stocks. If you own an actively-managed, large-cap mutual fund, it is almost certain that you own these stocks.

In other words, your position is shared by countless others, which means it is at risk if sentiment toward the stocks — and the sector — turns in a hurry like it did this past week with Facebook.

Accordingly, now is perhaps as good a time as any to check your exposure to the information technology sector, which accounts for roughly 26% of the S&P 500's market value.

Carrying even a market weight position leaves you at increased risk of a material loss if there is a shock to the financial market because fund managers and individual investors will sell what they can when there is a shock and not what they want.

These stocks and this sector is where the liquidity will be because they are so widely-owned. To that end, they can turn in a hurry from a source of wealth to a source of funds in fast-moving markets.

Eye Opening

We don't mean to create an impression that these stocks, this sector, and the market are about to implode. Rather, we mean to convey to readers that the Facebook experience should be an eye-opening one.

The stock lost 20% of its market value in a matter of minutes. If nothing else, that should make it apparent that the risk is high in owning concentrated positions — and even more so when a growth story has been called into question.

Rebalancing an investment portfolio is a prudent course of action and it doesn't always need to be reserved for an end-of-year exercise.

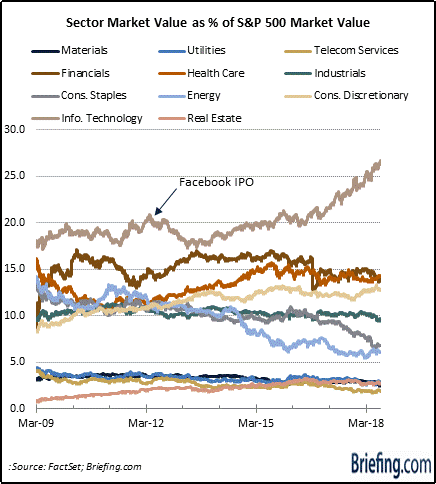

One can see in the chart below how the information technology sector has been the place to be for the most part during this bull market, which began in March 2009. It has certainly been the must-own sector over the past five years when stocks like Apple, Alphabet, Facebook, Microsoft (MSFT), and NVIDIA (NVDA) have run nearly uninterrupted — and not exactly without reason either.

Valuations in many instances, however, have gotten stretched along with the stock prices. That has been owed in part to the persistence of ultra-low interest rates, yet the Federal Reserve is working to change that.

Consequently, there is a reason to think the "easy money" has been made now that interest rates are rising, the law of large numbers and challenging comparisons are catching up to the mega-cap leaders, and a stronger dollar, protectionist trade measures, and rising labor costs are presenting some growth headwinds.

What It All Means

The information technology sector is a monolith of sorts. It will continue to stand as a monument of the future, which is why it should always hold investment appeal for long-term investors.

Growth is concentrated in that sector, but as this article has alluded, there is a lot of investment interest concentrated in the information technology at this time and particularly among its mega-cap leaders.

That creates added price risk when things go awry, especially if an investment portfolio isn't balanced to mitigate the price risk of a high-flying sector.

There are other investment options out there to consider, many of which have taken a backseat to the crowded position in the front seat that has been occupied by the information technology sector.

While all sectors have risen with this bull market tide, many have been left behind in the big wave of interest in the information technology sector.

The table below shows where the 11 economic sectors stand today as a percentage of the S&P 500's market value versus where they stood on March 6, 2009.

Source: FactSet

It may come as a little surprise to see that the weighting of the counter-cyclical sectors (consumer staples, healthcare, telecom services, and utilities) is lower today than it was then since it has been a predominately risk-on market in the interim.

That may be eye-opening in its own right, as market pundits banter about the prospect of reaching peak economically, and earnings, growth, and how the flattening yield curve and the underperformance of copper prices could be signaling more challenging economic times ahead.

The future will make it all plain to see eventually.

Checking your exposure to a widely-owned information technology sector today, though, could pave the way to a rebalancing exercise that creates a better overall risk-reward balance than what hit a lot of investors squarely in the face(book) this past week.