Originally posted at Briefing.com

It's the dead of summer right now, which means the heat is on throughout the country. Somewhere else things are hot — and getting hotter — is the financial markets.

The heat in the financial markets, however, isn't necessarily like the heat we equate with good summer times. Rather, it's more like the heat we equate with a rising temperature brought on by a virus.

Developing Symptoms

The financial market hasn't caught a cold just yet, yet there are a lot of developing symptoms of a longer-lasting malady that are being dismissed as if they are nothing more than a 24-hour flu.

Actual Tariffs and the Threat of More Tariffs

The tariff ball got rolling with the U.S. imposing steel and aluminum tariffs and it has kept bouncing with the implementation of tariffs on $34 billion worth of imported Chinese goods, the impending imposition of tariffs on another $16 billion worth of Chinese goods, the consideration of a proposal to slap a 25% tariff on another $200 billion worth of Chinese goods, versus an originally proposed 10% tariff, and the overarching threat to impose a tariff on all $500 billion worth of imported Chinese goods.

Read Is a Summer Swoon Emerging?

Some of the auto tariff angst related to U.S. dealings with the EU have died down after the meeting between European Commission President Juncker and President Trump, yet nothing has been settled there, so it's another potentially harmful tariff action that continues to hang in the balance.

The stock market has bobbed and weaved on the pugilistic trade headlines, yet with the S&P 500 up 6.2% year-to-date and roughly 1.1% shy of its all-time high, it is fair to say that it thinks these trade spats aren't going to kill the bull market.

Ongoing Yuan Weakness

Is the weakness in the Chinese yuan a tacit devaluation by the Chinese government to offset the negative impact of tariffs or is it the byproduct of a weakening economy that is driving capital offshore?

It may be both. The important consideration is that the yuan is weakening — and it isn't for good reasons no matter how one views it.

Read Chris Puplava: Near-Term Weakness, Overheating in 2019

That weakening, if it continues, is going to heighten the potential for competitive devaluations, as other countries seek to defend their export share, and the potential for more competitive trade action by the Trump Administration if a stronger dollar threatens the U.S.'s export share and leads to a widening in the trade deficit.

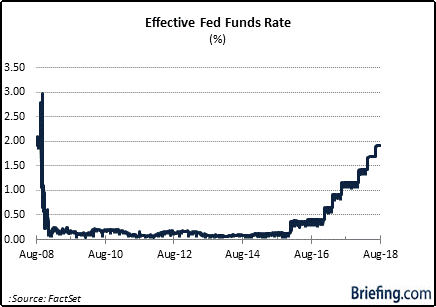

The Federal Reserve Is Reining in Its Policy Accommodation

The Federal Reserve is simultaneously shrinking its balance sheet and raising the target range for the fed funds rate, thereby driving up the cost of credit that is making it less affordable for borrowers to take on debt, and to repay variable rate debt, and more expensive for companies to service their debt.

The Federal Reserve has maintained that its rate-hike approach is likely to be a gradual one, yet every increment of 25 basis points counts as a brake of sorts on the economy.

Interest rates are still relatively low, but they are rising, which means they are less accommodative than before and create some refinancing risk for consumers/corporations that find themselves in a position to refinance existing debt. The latter is no small consideration given the research from S&P Global that suggests U.S. corporate debt is at a record .3 trillion.

Risk-free Competition for Stocks Is Rising

The dividend yield on the S&P 500 is 1.99%. The yield on the 3-month T-bill is 2.01% while the yield on the 2-year Treasury note, which is sensitive to changes in the fed funds rate, is 2.64%.

With the Federal Reserve raising interest rates, income-oriented investors have some risk-free alternatives that are stacking up as well as they have in some time (i.e. the best in about 10 years) versus riskier alternatives. In other words, the stock market is starting to be confronted with the reality that it isn't the only game in town anymore.

The Budget Deficit Is Rising

The tax cuts have bolstered economic activity, and thus far they have also bolstered the budget deficit along with defense spending and entitlement program costs.

The tax cuts were sold as something that will pay for themselves through increased economic growth, yet that promise is still elusive, evidenced by the Treasury Department's recent announcement that it will be increasing its debt issuance in the third quarter to 9 billion from an April estimate of 3 billion. The delta there is billion, which is striking knowing the U.S. economy just posted its strongest growth rate since the third quarter of 2014.

The fiscal year-to-date budget deficit is 7.1 billion versus 3.1 billion at the same time a year ago. It is estimated that the FY18 deficit will reach 3 billion, or 4.2% of GDP, versus 5 billion, or 3.4% of GDP in FY17.

The deficit trend is moving in the wrong direction and the Congressional Budget Office estimates federal deficits will average .2 trillion per year over the 2019-2028 period, assuming current tax and spending laws remain unchanged. As a percent of GDP, the deficit increases from 3.5% in 2017 to 5.4% in 2022 versus an average annual deficit of 2.9% over the past 50 years.

The implication is that increased borrowing needs could ultimately be met with an increased demand for higher interest rates to compensate creditors for taking on the debt. Higher rates, as noted above, impede economic growth and pose competition for stocks.

Eye-Opening Fallout in Facebook's Stock Price

After shocking investors with a sharp cut to its operating margin guidance, shares of Facebook (FB) plunged 20% in a matter of minutes. While the stock has stabilized in recent sessions, the speed with which the stock dropped should have been a warning to all invested in "crowded stocks" and "crowded ETFs" just how quickly things can change in a programmatic market.

Facebook's issue was a company-specific one, yet its experience was representative of how market mechanics can get out of whack in a hurry when event risk hits and liquidity is constrained.

On another level, the fallout in Facebook provided an indelible reminder to investors to check their exposure to the information technology sector to determine if it might be prudent to do some rebalancing.

The CBOE Volatility Index Is Backing Up as Stock Prices Keep Rising

It's misleading to say there is no fear in the market, yet the CBOE Volatility Index ("VIX") is leading us to assert that there is less fear in the market despite the trade issues, the weakness in the yuan, rising interest rates, a rising budget deficit, and Facebook's fallout.

The drop in the VIX reflects a favorable near-term outlook. Some might say it reflects some concerning complacency has given the seeming lack of interest in hedging portfolios for near-term downside risk.

A low level in the VIX Index isn't necessarily a contrarian indicator. It simply suggests that there is a relative lack of defensive positioning overall that could hit hard if there was a shock to the stock market.

What It All Means

The stock market has shown some impressive resolve in the face of some adverse developments, underpinned by strong earnings growth and an abiding belief (it would seem) that the trade issues won't cause undue economic harm.

In a manner of speaking, the market's immune system has remained strong. Even so, a nasty virus can pop up suddenly and compromise that immune system.

When one feels some cold symptoms coming on, they can take various steps to try to keep the virus from getting worse. Staying hydrated, getting good rest, and taking some over-the-counter medicine are some defensive-minded approaches aimed at keeping that virus from getting the best of you.

In the same vein, investors should recognize that there are germs out there that risk compromising the market's immune system.

Things look hot now with the Nasdaq Composite up 13.2% year-to-date, the Russell 2000 up 9.0%, and the S&P 500 up 6.2%, yet steps can be taken to mitigate the risk of suffering a nasty virus, including reducing exposure to stocks that have made outsized moves, rotating funds into lower-beta sectors like health care, consumer staples, utilities, and telecom services, and improving liquidity by raising cash levels and/or favoring shorter-dated Treasury securities.

Yes, stock prices are rising but temperatures are, too.