Originally published at The Boock Report

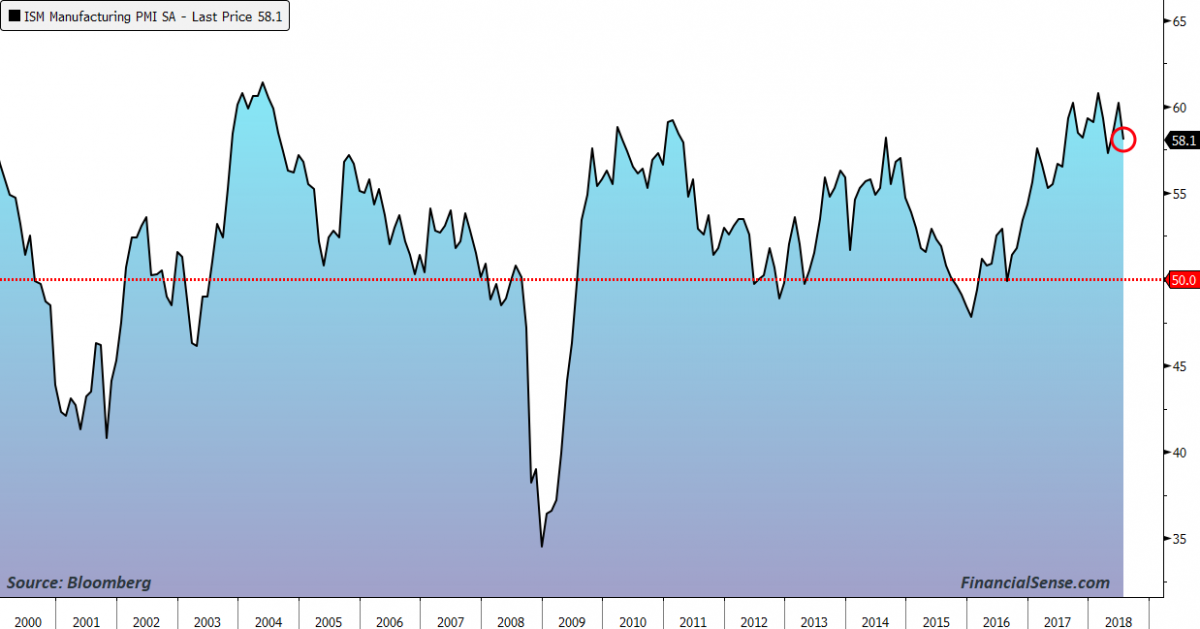

The US ISM manufacturing index for July moderated by 2.1 pts to 58.1 which is a 3 month low and puts it below the average year to date of 59.1. Of note, new orders fell 3.8 pts to 60.2, the lowest since May 2017, backlogs dropped by 5.4 pts to 54.7, the least since November 2017 and export orders fell 1 pt to the slowest since October 2017. Supplier deliveries did ease by 6.1 pts but after rising by a like amount in June. Inventories at the manufacturing level did rise to a 4 month high but remained extremely lean for customers. Prices paid did moderate by 3.6 pts to the lowest since January but remains very elevated at 73.2 (50 is breakeven). Employment held steady, rising by .5 pt to 56.5 which is in line with the 6 month average of 56.7.

Don't miss Tariffs Mean Less Economic Growth, More Inflation, Says Peter Boockvar

While we did see the headline drop, the number of industries reporting growth did remain at 17 of 18 surveyed.

The ISM summed up the report with the positives and negatives that we are all aware of, “Demand remains robust, but the nation’s employment resources and supply chains continue to struggle. Respondents are again overwhelmingly concerned about how tariff related activity, including reciprocal tariffs, will continue to affect their business.” I don’t need to add anything more. US Treasuries didn’t rebound on the headline miss, yields remain at the high of the day with the 10 yr sitting right on 3.0%.

Here are comments on this straight from the horse’s mouth, American business:

“Global demand is still strong. Working on contingency plans for the Chinese tariffs. We will probably onshore most of that material. Labor availability is becoming an issue.” (Computer & Electronic Products)

“As a result of new tariffs on materials to/from China, we are taking measures to move impacted materials ahead of effective dates, which in some cases is resulting in holding higher inventories.” (Chemical Products)

“Steel cost increases are causing a lot of negotiations. The increases are real and will affect costs beginning in the third quarter of 2018.” (Electrical Equipment, Appliances & Components)

“Reviewing the business case for importing manufactured parts from China, as new tariffs will lead to increased costs that we will pass along to our domestic customers.” (Transportation Equipment)

“Corn and soybean meal costs are reducing. Labor continues to be a struggle to fill open positions.” (Food, Beverage & Tobacco Products)

“The steel tariffs are a concern to us. We have already seen steel prices increase due to the threat of the tariffs and are seeing kickback from our customers due to the higher prices. We are concerned that the end customer will go to off shore to purchase the finished product.” (Fabricated Metal Products)

“Business is moving along at a brisk pace, outperforming the annual plan year-to-date (calendar year financials). However, internationally, nationally and locally, we are finding many manufacturers behind schedule due to capacity constraints. They are stating their order intake is heavy and/or they cannot find qualified employees to get all the work done.” (Machinery)

“Tariffs are [resulting in] customs inspection-time increases on imported raw materials from China. Logistics seems to be improving, but we are seeing a [continuing] tight chemical bulk tanker market.” (Plastics & Rubber Products)

"Our customer demand is high, but supply of aluminum is tight. Also, tariffs are negatively affecting our bottom line, as we are unable to pass increases to all of our customers. Plus, we are seeing increases in our construction costs because of the steel price increases. Labor market is extremely tight for professional personnel, plant technicians and support associates.” (Primary Metals)

“The so-called trade war is now taking its toll on business activity, resulting in substantial reductions to new export orders. China has all but stopped taking orders, causing inventories to build up in the U.S. Domestic business is steady. However, it is too small to carry the load that export markets have retreated from. As a result, we will be meeting as a corporation next week to recast our second-half sales and revenue projections.” (Wood Products)

For daily macroeconomic analysis and asset class positioning, visit boockreport.com