Today Fed Chair Janet Yellen gave a speech at the “Designing Resilient Monetary Policy Frameworks for the Future,” symposium in Jackson Hole, Wyoming.

Her speech was on The Federal Reserve’s Monetary Policy Toolkit: Past, Present, and Future.

“I believe the case for an increase in the federal funds rate has strengthened in recent months. Of course, our decisions always depend on the degree to which incoming data continues to confirm the Committee’s outlook,” said Yellen.

As usual, the word “uncertainty” was prominent in the discussion.

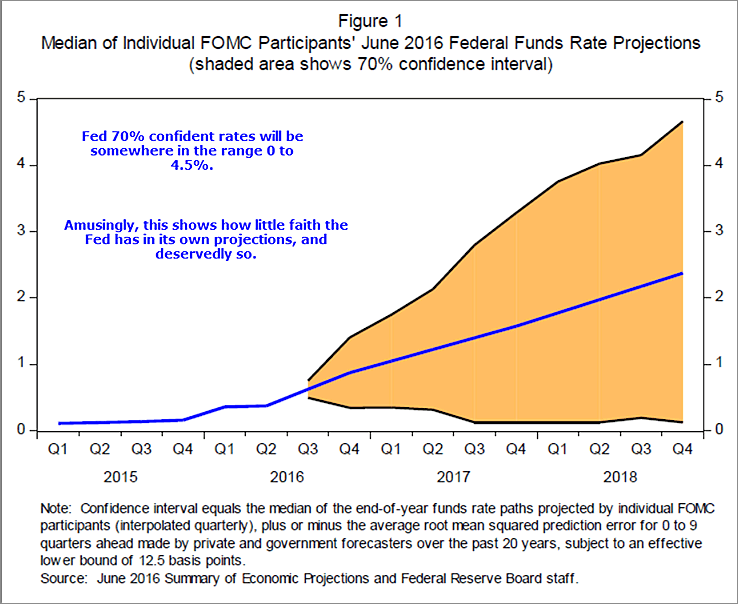

And, as ever, the economic outlook is uncertain, and so monetary policy is not on a preset course. Our ability to predict how the federal funds rate will evolve over time is quite limited because monetary policy will need to respond to whatever disturbances may buffet the economy. In addition, the level of short-term interest rates consistent with the dual mandate varies over time in response to shifts in underlying economic conditions that are often evident only in hindsight. For these reasons, the range of reasonably likely outcomes for the federal funds rate is quite wide–a point illustrated by figure 1 in your handout.

Fed Confidence Levels

Amusingly, that slide shows how little faith the Fed has in its own projections, and deservedly so.

By some calculations, the real neutral rate is currently close to zero, and it could remain at this low level if we were to continue to see slow productivity growth and high global saving. If so, then the average level of the nominal federal funds rate down the road might turn out to be only 2 percent, implying that asset purchases and forward guidance might have to be pushed to extremes to compensate.

Asset purchases are not at an extreme already? Would it buy every bond like Japan? Here’s an amusing paragraph:

If future policymakers responded to a severe recession by announcing their intention to keep the federal funds rate near zero for a very long time after the economy had substantially recovered and followed through on that guidance, then they might inadvertently encourage excessive risk-taking and so undermine financial stability.

Read Acampora: With Rates at These Levels, Stocks May Have Years Left to Run

Hello Janet, wake up! You are talking about the future. But we are there already there.

On the monetary policy side, future policymakers might choose to consider some additional tools that have been employed by other central banks, though adding them to our toolkit would require a very careful weighing of costs and benefits and, in some cases, could require legislation. For example, future policymakers may wish to explore the possibility of purchasing a broader range of assets. Beyond that, some observers have suggested raising the FOMC’s 2 percent inflation objective or implementing policy through alternative monetary policy frameworks, such as price-level or nominal GDP targeting. I should stress, however, that the FOMC is not actively considering these additional tools and policy frameworks, although they are important subjects for research.

Beyond monetary policy, fiscal policy has traditionally played an important role in dealing with severe economic downturns. A wide range of possible fiscal policy tools and approaches could enhance the cyclical stability of the economy.25 For example, steps could be taken to increase the effectiveness of the automatic stabilizers, and some economists have proposed that greater fiscal support could be usefully provided to state and local governments during recessions. As always, it would be important to ensure that any fiscal policy changes did not compromise long-run fiscal sustainability.

Conclusion

Although fiscal policies and structural reforms can play an important role in strengthening the U.S. economy, my primary message today is that I expect monetary policy will continue to play a vital part in promoting a stable and healthy economy. New policy tools, which helped the Federal Reserve respond to the financial crisis and Great Recession, are likely to remain useful in dealing with future downturns. Additional tools may be needed and will be the subject of research and debate. But even if average interest rates remain lower than in the past, I believe that monetary policy will, under most conditions, be able to respond effectively.

Yellen sounds clueless as ever.